All Boats Rise as Theatrical, Transactional and Streaming Grow

Transactional a ‘Vital Value Bridge’ from Cinema to Streaming

- An unprecedented period of change delivers a fresh entertainment industry model for the future: the value of the UK Screen Industry in 2025 increased by 5.4% to £13.3bn, with Streaming (Subscription Video on Demand or SVoD) and Premium Advertising-based Video on Demand (AVOD) more than compensating for the decline in the value of traditional pay TV, as Cinema continues its growth back to its 2019 value levels post the global pandemic and writers strikes

- The value of the global media and entertainment industry is US$1.1tn, up 7% from 2024, according to global insights provider Omdia

- Global Video Entertainment is now a $349bn consumer market. The US remains the biggest single market but ‘International’ now represents 60% of that number

- The global Box Office is projected to reach $35bn in 2026 (+5 % YoY)

- UK Digital transactional formats are forecast to grow 3.6% in value this year, with EST movies up 7% in value in the UK

- Savvy consumers, entertainment partnerships and commercial innovation fuel global momentum as Home Entertainment redefines the value of the international market, where the international transactional category is growing faster and is higher in value than the traditionally dominant US market

- The UK leads the way: record UK performance sees the UK Media & Entertainment market reach an all‑time high of £34bn (+8 % YoY), with the Home Entertainment sector rising 10% YoY to £5.7bn, the largest value number in recorded history

- Fresh data highlights the commercial innovation driving success across multiple international markets through ad tiers: 23 million UK ad-supported streaming subscriptions in 2025 play a key role in the growth of the value of the sector

- Innovative pricing and windowing strategies result in ‘premium’ growth and success: 79 ‘Premium’ titles were released fresh from cinema at a higher initial price on both Premium electronic sell-through (PEST) and Premium video on demand (PVoD) driving value success for the sector and reinforcing the importance of transactional as a vital value bridge between the theatrical and streaming models

- Theatrical and Home Entertainment embrace partnership in clear acknowledgment of consumer demands and behaviours: streaming giant NETFLIX eventises the final episode of STRANGER THINGS in a day-and-date New Years Eve and New Years Day cinema release, while industry-first promotion GO BIG AND GO HOME in the UK opens a new frontier of exhibition and transactional partnership as ODEON and Amazon Prime Video join forces for the first time to reward audiences

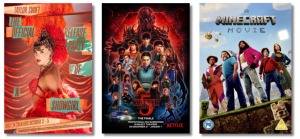

- Original IP spells success for a selection of titles as consumer appetite remains for new stories: Universal Pictures’ WICKED and WICKED: FOR GOOD, Warner Bros Discovery’s A MINECRAFT Movie and SINNERS, and British StudioCanal title I SWEAR demonstrate the impact of new stories across the entertainment lifecycle

- Universal Pictures was the UK’s largest theatrical distributor in the UK in 2025, and the UK’s largest Home Entertainment distributor with a 17.8% market share of Home Entertainment, followed closely by Warner Home Video (17%) as talks of its potential sale to Netflix continue

January 29th 2026: Today, market reporting and analysis from the British Association for Screen Entertainment (BASE) and Digital Entertainment Group International (DEGI), in association with the market leading insight providers in UK and international entertainment reveal the scale of the success of the global screen entertainment industry in 2025.

The UK entertainment industry delivered a record‑breaking year in 2025 with total market value reaching £34bn ($46.9bn), an 8% increase on 2024 (includes streaming, transactional and Pay TV Home Entertainment, Cinema, Games, and Music). Visual Home Entertainment consumer spend accounted for 17% of that number.

Global Home Entertainment is now a $349bn consumer market according to NBCUniversal Internal Analysis using data from key partner insight providers. While the US remains the largest individual territory, international markets are now driving the majority of global value, accounting for around 60% of total video revenue, and growing materially faster than domestic markets. This growth is coming from markets such as India, Poland, the Netherlands and parts of APAC significantly outpacing mature territories. At the same time, established markets such as Japan demonstrate the enduring value of strong local content, while newer platform entry in markets including Poland and the Nordics has delivered incremental growth by expanding access and choice. Together, these dynamics reinforce the importance of international, market-specific strategies as a central driver of future industry growth.

The value of the Home Entertainment market in the UK rose by a massive 10% year on year to an all-time high of £5.7bn, which includes streaming, buying, and renting films and TV shows. The scale of this success in the UK reflects Britain’s status as one of the world’s most advanced and dynamic screen‑consumption markets, with a particularly innovative and forward-thinking category open to collaboration and innovation. The results reflect the potential of the international Home Entertainment sector, and the growing momentum for the Home Entertainment category as consumers favoured visual entertainment format.

Worldwide, the entertainment industry recorded its strongest expansion since 2019. Gower Street Analytics forecasts the global Box Office at $35bn in 2026, up 5% year-on-year (YoY), a second consecutive year of positive growth for cinemas, which remain a vital first platform for transactional Home Entertainment. The International market (excluding China) is predicted to finish 5% ahead of 2025 (est.) at approximately $18bn. Regional outlooks remain buoyant: the North America Box Office is set to grow +11% in 2026, with Latin America +9%, and EMEA +7% at a value of $10.05bn.

Streaming dominated consumption with 20.3mn UK households subscribed to at least one streaming service, an increase of nearly half a million YoY, where nearly 70% of viewers watching streamed content. Netflix led the UK market with 17.6mn home subscriptions where WEDNESDAY was reported to be the most popular show, followed by Amazon Prime Video with 13.6mn, and Disney+ with 7.5mn. There was also noted market percentage growth for Discovery, which grew to 3.2mn home subscriptions, Apple TV which grew to 2.8mn home subscriptions, and NOW which grew to 2mn home subscriptions.

At the same time, ad-supported streaming models accelerated adoption worldwide. The UK alone reached 23mn ad-supported subscriptions by Q3 2025 where 53% of all SVoD subscriptions are now ad-supported. Digital i reports that 40% of Netflix’s global users and 44% of Disney+ subscribers now engage with ad‑tier plans. One third of new UK SVoD subscriptions are now ‘bundled’; taken through partner platforms including traditional Pay TV, broadband and mobile network providers, online channel platforms such as Amazon Channels, Apple Channels, and YouTube Primetime Channels. The launch of HBO Max in the UK in 2026, and the return of fan favourites such as FRIENDS to UK SVoD audiences, is predicted to drive more change in the market.

Max Signorelli, Consumer Research Lead, Media & Entertainment, Omdia, said: “Consumer expectations of their media services are rising in tandem with their still increasing spend. Although near invisible and seamless to the consumer, the media and entertainment partnerships and distribution channels that increasingly define the global industry are more relevant and powerful than ever before. Particular investment priorities will include new, international productions and formats (K-wave, microdramas etc.), content discovery (TV platform and AI-enhanced search) and enhanced, intertwining features (cross-platform productions and shoppable TV).”

58% of UK adults now pay for at least one streaming service with ads despite 55% of consumers reporting that they dislike ads but prioritise the cost savings. Prime Video secured 17% of new paid sign-ups (both ad-supported and non-ad-supported) narrowly ahead of Disney+ at 16%.

Fabric reports that 69% of UK SVoD users prefer to spend less on an SVoD plan with ads, showing the option to pick a lower‑cost subscription model drives incremental revenue and widens access for consumers. This number is significantly higher in the UK than Australia where 58% of users say they opt for a lower cost plan with ads. Italy demonstrates a particularly high preference for ad-supported tiers at 73% of all users, spotlighting clear regional differences and further room for growth in ad-supported markets.

Live and event-based streaming supported growth. Netflix’s 2025 Christmas NFL GameDay broadcast delivered its largest US sign‑up surge of the year coupled with the STRANGER THINGS season 5: THE FINALE simultaneous cinema and streaming release, demonstrating the new hybrid potential of “eventised” home viewing, driving 430,000 new US subscriptions. Live events generated 60% of major SVoD sign-up peaks, delivering stronger ad-tier adoption across platforms. The highly publicised STRANGER THINGS: THE FINALE aired in approximately 600 cinemas in the US alone, achieving upwards of $25mn of ‘concession cash’ for movie theatres over New Year’s Eve and New Year’s Day. At the beginning of 2026 Netflix reported 325mn global paid subscribers, with full year ad-revenue growth up more than 2.5 times to over $1.5bn, and combined revenue up 18% YoY.

Taylor Swifts: THE OFFICAL RELEASE PARTY OF A SHOWGIRL was in cinemas for one weekend only from 3-5th October 2025, grossing $34mn at the US Box Office and $50mn worldwide.

7% of UK sports rights spend in 2025 came from Subscription Streamers, an increase in share of nearly 70% on 2024. An average of 20% of global sports rights spend is from dedicated subscription streamers, but important deals such as that signed by Paramount last year for the UK rights to the Men’s Champions League coverage (beginning in 2027) will shift the dynamics of the UK market. DAZN also achieved record subscriber numbers driven by interest in the FIFA World Cup.

Transactional entertainment (buying and renting, either on digital or physical) continues to play a vital role in maintaining revenue continuity across the release lifecycle. Premium VoD (PVoD), Premium EST (PEST), standard EST/VoD, Blu‑ray and DVD together form the commercial bridge between cinema and subscription monetisation, giving audiences choice while sustaining robust returns for studios and distributors.

In 2025, a record 79 films were released “fresh from cinemas,” up from 62 titles in 2024. Premium content now accounts for more than 20% of transactional spending and this share is set to rise in 2026 to around 25%, supporting a forecasted growth rate of 4%.

Craig Armer, Global Strategic Insight Director, Worldpanel by Numerator, said: “There are now more British households using VOD services than ever before, driven by the success of Ad-Supported Tiers in the SVoD category providing an accessible price point for new consumers. Worldpanel’s new monthly tracking of consumer engagement with transactional digital formats indicates that this audience is also in growth, with over 5mn British adults purchasing at least once in the nine months to December 2025. Transactional consumers generate important incremental revenue for Home Entertainment, as the average transactor is already very engaged with the wider VoD category. Occasions such as movies nights with the family, or unwinding by watching a film, are times when consumers choose to buy or rent in addition to their subscriptions. Positively, there is still plenty of headroom for further growth. Understanding which VoD consumers could be converted into transactional, and how to do this effectively, will be essential to carry this year’s performance into 2026.”

The average Theatrical-to-Premium window stood at 44 days, 10% longer than the 40-day window of 2024. An average additional 40-day window follows to standard EST, just one day less than in 2024, as settling windowing strategies prove effective in both driving Theatrical attendance and maximising digital value. Titles such as WICKED, GLADIATOR II, CONCLAVE, DOWNTON ABBEY: THE FINALE, and SUPERMAN (2025) demonstrated early premium availability strengthening both audience engagement and long‑tail revenues.

Digital transactional formats continued to expand in line with savvy consumer understanding of availability; electronic-sell-through (EST) grew 7.4% in value, and digital rentals increased by 1.7%. The combined digital sales market rose 3.5% to a value of £382mn, while the combined UK transactional market (physical and digital) rose by 1% to reach £531mn. This UK transactional market growth is even more impressive when viewed alongside the UK box office figure, which grew by 1%.

Futuresource forecast digital transactional to grow 3.6% YoY in value in 2026, driven by value growth in EST movies in particular which are expected to grow another 7% YoY in value, and now account for more than 53% of this spend. Futuresource Screen Trends highlights the UK as the third largest market behind only the United States and Germany, although those markets recorded a slightly softer lift of 2.9% in total transactional spend for digital buying and renting compared to 2024.

James Duvall, Principal Analyst at Futuresource Consulting, said; “2025 has proved to be another year where the UK transactional sector has played an important role in engaging audiences, and the outlook for 2026 is extremely promising.”

The final week alone of 2025 saw 2.2mn unit sales and rentals. Physical formats remained resilient, and the choice of many consumers. Blu‑ray value was up 3.2% YoY, led by SUPERMAN (2025), which was the number one title on the Official Blu-Ray chart. The value of the 4k Blu-ray market grew 19.5% YoY as collectors swooped on limited editions and high value SteelBooks: only 10% of all 4k Blu-ray titles had a SteelBook edition, but the sales of SteelBooks made up 18% of the total Blu-ray 4k revenue number, with an average consumer retail price of £32 per unit.

DOWNTON ABBEY: THE FINALE reminded retailers of the strength of the DVD market selling 56 000 DVD units in its first two weeks of release in December 2025. Four of the five top selling TV Titles in 2025 first aired on streaming channels in the UK where HBO’s HOUSE OF THE DRAGON dominated for the third year running, and fan favourite Doctor Who took the number two spot with the classic DOCTOR WHO: THE SAVAGES, which first aired in 1966.

UK creativity underpinned performance across the global slate. British‑backed productions including Universal Pictures WICKED and WICKED: FOR GOOD, GLADIATOR II, CONCLAVE, BRIDGET JONES: MAD ABOUT THE BOY, THE SUBSTANCE, and JURASSIC WORLD: REBIRTH, dominated Official Charts Company rankings and reinforced the UK’s role as a global production leader.

Original IP played an important role for audiences in 2025 demonstrating appetite for new stories and success across the entertainment life-cycle. Warner Bros Discovery release A MINECRAFT MOVIE delivered a UK Box Office of £56.5mn which converted to a value of £7mn across EST and VoD, while SINNERS – now the most Academy Award® nominated film of all time- delivered £16.1mn at the UK Box Office and £3.2mn across VoD and EST. StudioCanal’s October 2025 theatrical hit I SWEAR demonstrated the impact of new stories across the entertainment lifecycle with a £6mn UK Box Office converting to a Premium EST and VoD release in November 2025 that generated value of £584k.

Looking forwards, across 2026 and beyond, both transactional and subscription models will continue their formidable growth surge if market and cultural conditions remain stable. Futuresource forecasts 3.6% digital growth for UK Home Entertainment, with EST titles increasing 7% in value in the UK, confirming sustained consumer enthusiasm for Premium ownership experiences.

Stabilised window models will provide clear pathways from Theatrical to Premium to standard digital and physical formats, anchoring predictable returns for content-creators and rights‑holders. 2026 will also see further experimentation with live-event streaming and curated content discovery from the likes of LETTERBOXD Video Store which launched in December 2025. Audience attitudes towards a preference for human curation over algorithmic recommendation will continue to evolve, influencing platform design, introducing new players to the market, and renewing interest in nostalgia and franchise storytelling. The theatrical release of TOY STORY 5, THE DEVIL WEARS PRADA 2, and STAR WARS’ next chapter will not only strengthen the global Box Office but both the transactional and streaming channels, where complimentary release models drive drafting success and post-theatrical success across all channels.

Universal Pictures was the UK’s largest Theatrical and Home Entertainment distributor in the UK in 2025, with a 17.8% Home Entertainment market share, followed closely by Warner Home Video (17%) led by 2025 BOX OFFICE number one A MINECRAFT MOVIE, which netted £56.9mn at the UK Box Office.

Cross-platform and channel partnerships like ODEON and Prime Video’s GO BIG AND GO HOME will continue to innovate the sector, forging even closer ties between the theatrical and Home Entertainment estates, delivering increased value perception for distributors, retailers and exhibitors, and discount rewards for entertainment consumers.

Yasmin Nevard, Head of Insights at BASE and DEGI, said: “As we look back across 2025 and into 2026, the direction of travel for the screen entertainment industry is clear: growth is being driven not by a single model, but by how well different models work together. Our data consistently shows that theatrical, transactional and streaming are most powerful when they are complementary rather than competitive, with transactional continuing to act as a vital value bridge, extending engagement and sustaining revenue across the release lifecycle. Underpinning this growth are significant shifts in both the market and consumer behaviour. Changes to windowing, pricing, distribution and partnership models are reshaping how and when audiences engage with content, while viewing habits, discovery pathways, and expectations of ease continue to fragment. Understanding the full consumer journey, and where these market shifts create friction or opportunity, has become increasingly complex and important. Technology, including AI-driven curation and recommendations, will play a role in responding to this, but it is clarity of insight that will determine success. At BASE and DEGI our role is to bring that clarity. By combining robust market data with a deeper understanding of audience attitudes and behaviours, we are developing a more nuanced segmentation that moves beyond broad demographics and reflects how people actually engage with film and television. Alongside this segmentation work our broader insight programme draws on international perspective and learning from adjacent industries to help members identify real growth opportunities, sharpen discovery, and apply innovation, including AI, in ways that are effective, responsible and commercially meaningful.”

Social‑video platforms remain a growth engine. YouTube contributed £1.5bn to the UK video economy and was the most widely used streaming video service in the UK last year, with 66% of UK Internet users engaged with YouTube monthly, and 41% daily. Over half of the UK population aged 18-54 watch YouTube daily where usage is highest amongst 18-34 year olds.

Global social-video value on social media platforms was worth £8.5bn in 2025, where 29% of internet users used TikTok monthly, and 19% daily. $32.5bn was spent in 2025 globally on influencer marketing (brand budgets paid to creators and campaigns around social platforms), up a significant 35% from $24bn in 2024. These numbers underscore the expanding role of creator‑driven content in today’s entertainment landscape and the importance of future collaboration across the Home Entertainment sector, where the BBC recently announced original programming for the channel in 2026, and where transactional Home Entertainment will continue to make partnership strides in 2026.

Liz Bales, Chief Executive of BASE and DEGI, said: “2025 was a landmark year for UK and International Home Entertainment, and the global entertainment industry stands united behind creativity and commercial innovation. In the UK we are a sector evolving at lightning speed with strength and agility, powered by collaboration. As we move into 2026 the next chapter of this exciting industry story is being written. With stable market conditions, revenues across cinema, physical, and digital platforms will continue to grow confirming that consumers value choice, and that diversified release strategies deliver consistent, sustainable growth. Audiences will continue to engage passionately with great stories if we continue to deliver them in exciting ways that match the pace and reality of their lives. I want to thank all the UK and International BASE and DEGI Members for their partnership and vision in 2025, and their belief in what can be this year and next. We are now a force of over 100 Member and partner organisations and these results clearly show that together we are stronger.”